I Owe the IRS Back Taxes HELP!

- Posted by Joshua Sells

- On April 19, 2021

- IRS Back Taxes, IRS Tax Attorney, IRS Tax Debt, IRS Tax Relief, Offer in Compromise, Ohio Tax Attorney, Tax Settlement

Getting a notice in the mail that you owe the IRS back taxes is scary. That moment when you say to yourself, “I owe the IRS back taxes” and you don’t even open the envelope because you already know what is inside. You may feel like you are alone and have no way out – after all, it is the IRS – one of the most powerful governmental agencies on the planet. For many, the back tax problem has been compounding for years. For some, this is the first time that you have been on the IRS radar.

Regardless, you’re not alone. In 2019, over 11 million taxpayers owed IRS back taxes.

Maybe you are scarred spitless – not even knowing what to do next. Or maybe you think the IRS will just forget about you if you forget about the. Let me assure you, the IRS has the resources and tools available to come at you with the full might of the United States government. Usually, when the CP504 notices go out (threatening asset seizures), that is when taxpayers begin to call me saying, “I owe the IRS back taxes HELP.” If that is you, don’t bury your head in the sand – you do have options to deal with your IRS back tax.

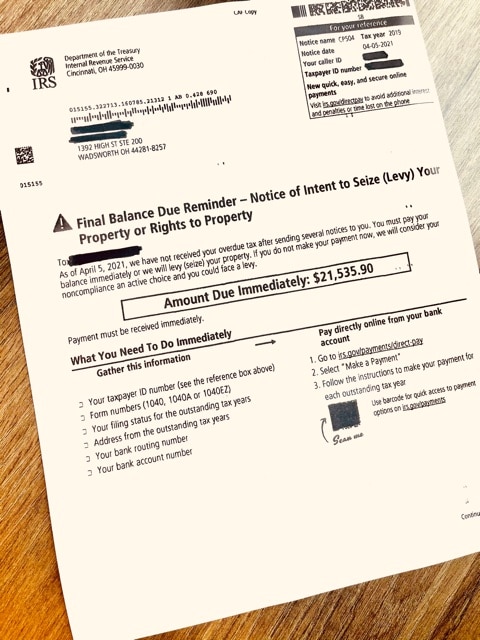

CP 504 Notice IRS Balance Due Notice of Intent to Levy

What can the IRS do to me if I owe IRS back taxes?

With a 2019 budget of $11.8 billion and 73,554 full-time employees, the IRS has plenty of resources to collect back tax. Specifically, the IRS may choose to do any of the following to collect tax debt owed to it.

- File a notice of federal tax lien against in the public record to notify your creditors of your tax debt – this is a legal claim to your property and it may affect your ability to obtain credit.

- Seize and sell your property such as cars, boats, guns, jewelry, artwork, or real estate.

- Garnish your wages, social security benefits, retirement income, or 1099 income.

- Levy and take your bank accounts – they will literally wipe your balances out and there is little you can do to stop them.

- File civil cases in Federal District Court through the Department of Justice.

- Make criminal referrals to the Department of Justice in certain situations.

What can I do if I owe the IRS back taxes?

Offer in Compromise IRS Back Tax Settlement

An IRS offer in compromise allows you to settle your back tax debt for less than the full amount you owe. The IRS will consider an offer amount based on your income, expenses, and asset equity. Before you submit an offer in compromise, you must ensure that you have filed all required tax returns. If you are self-employed, you must also be current with any required estimated tax payments. If you are in active bankruptcy, you are ineligible to file an offer in compromise until the bankruptcy proceeding are closed. The IRS has a useful tool to see if you are eligible for an offer in compromise based on your income, expenses, and asset equity.

It is important to understand that the offer in compromise process is strictly a “mathematical process” that is based on your ability to pay (i.e. your income and expenses) and your available asset equity. It is not a “negotiation over the phone” and it is not a quick process. The typical offer in compromise will take 9-14 months from start to finish, assuming the IRS accepts your offer and you do not need to appeal a rejection.

If you are going to submit an offer in compromise in an attempt to settle your back tax, you will need two forms: IRS 433-A (OIC) and IRS 656. The IRS 433-A is the Collection Information Statement for Wage Earners and Self-Employed Individuals. This is the form that provides your full financial disclosure to the IRS, including your income, expenses, and assets. It is important that you understand a concept known as “Collection Financial Standards” before completing this form. For many household expenses (such as food, clothing, housing, utilities, out-of-pocket health care costs), the IRS will allow pre-determined monthly amounts (even if you don’t actually pay these amounts). You can increase the likelihood of an acceptance by understanding how to legally maximize your available household expenses.

The IRS 656 is the actual Offer in Compromise form that you will use to make your offer to the IRS. On this form, you have to identify the tax (and periods) that you want to include in your offer. Additionally, you will specify your offer amount and how you propose to pay the offer amount. An offer can either be paid as a lump sum (paid in 5 or fewer payments within 5 or fewer months of acceptance) or by period payment (paid in full between 6 to 24 months). Generally, you will be able to pay less by doing a lump sum offer.

Temporarily Delay IRS Back Tax Collection – Currently Not Collectible

If you are under a financial hardship (generally, this means that you have just enough income to handle your allowed household expenses), the IRS can “close” your collection account temporarily. The tax debt doesn’t go away – but the IRS will stop all collection activities against you while in this status (including garnishments). Generally, if the back tax is old, you may be able to stay in this “temporary” status all the way to the statute of limitations and the tax debt will be permanently written off by the IRS.

The statute of limitations is typically ten years from the date of assessment (this is also the date that your tax return is processed by the IRS). It is important to understand that the IRS can “check in” on you every couple of years to see if your financial situation has improved. The IRS will also take any tax refunds you are entitled to. To avoid this, make sure that you update your paycheck federal income tax withholdings to have less taken out each paycheck so that you have a minimal refund for the IRS to take.

With a “currently not collectible” status, the IRS will almost always file a tax lien against you. Unfortunately, there is not much you can do to avoid this if you are asking the IRS to temporarily delay collection efforts against you.

Long Term IRS Streamlined Installment Agreement

The IRS has payment plan arrangements that can be made to pay your back tax within an extended timeframe. The most popular payment plan with the IRS is the streamlined installment agreement. The payment plan is for 72 months and the payment amount is based on the assessed and accrued balance of your tax liability divided by 72. Generally, to get this amount, look at the last notice that you received (such as the CP504 notice). Take this amount (for each tax year that you have received a notice for) and divide by 72. That amount represents your monthly payment amount. You can even setup your installment agreement online through your IRS account.

The streamlined installment agreement is generally available for balances of $50,000 or less. If your balance is more than $50,000, but less than $250,000, you may still be able to setup an installment agreement without providing financial disclosures under the IRS COVID People First Initiative. Your proposed monthly payment amount, however, must full-pay the entire balance (including interest and penalties) before the statute of limitations date.

Once your installment agreement is established, consider requesting a first-time penalty abatement. You can save thousands of dollars this way. If you did not owe back tax for three years prior to the year that penalties were assessed for, you likely qualify for a first-time penalty abatement. You can ask for this over the phone with the IRS at 1-800-829-7650 – call early, though, as wait times generally exceed 1-2 hours.

Partial Payment Installment Agreement

If you do not qualify for a temporary delay in collection as “currently not collectible” and you cannot afford the streamlined installment agreement (i.e. the tax liability divided by 72), an alternative may be the partial payment installment agreement. Under this arrangement, the IRS will review your financial information (provided to the IRS generally through a 433-A or a 433-F) and determine what you are able to pay (including through any asset equity). Likely, under this arrangement, your monthly payment amount will never full pay the tax liability before the statute of limitations. At that point of time, the remaining tax balance will be written off by the IRS. It is possible to have a partial payment installment agreement for a large tax liability with a minimal monthly payment (we have seen them as low as $10.00 per month).

Under this arrangement, however, you have to ensure that you do not add additional back tax as it will cause your agreement to default. Similarly to the “currently not collectible” status, if you are due a tax refund, the IRS will take the tax refund, so you will want to adjust your withholdings so as to not have a tax refund.

Full Pay with Penalty Abatement

If you have the ability to full pay your back tax balance, then you likely to not qualify for any form of settlement, such as the offer in compromise. However, all is not lost. You can likely still save significant money in the form of tax penalties. As discussed above, if you had a clean compliance history for the preceding three years (from the year with the tax balance), you can simply call the IRS and ask them for a first-time abatement of your tax penalties for the year with the balance that you are full-paying. Technically, they will want you to full-pay the balance first and then request a refund through Form 843, but many of the agents will grant the first-time abate if they know you plan on full-paying your balance. Even if you do not qualify for first-time abatement, you may want to consider a “reasonable cause” abatement if there were good reasons why the tax was not paid on time.

Generally, tax penalties are well into the $1,000’s – sometimes more. It is important to note that interest cannot be abated – only penalties (such as the failure-to-file penalty and the failure-to-pay penalty). However, interest that has accrued on the penalties will be abated if a penalty abatement is granted.

If you are going to full-pay your IRS back tax balance, you should definitely send the payment electronically through the IRS Direct Pay website. Do not send a check as it is not reliable. If you must send a check (again – not recommended), make sure that your social security number and the tax year you want to apply the payment to is on the memo line of the check.

If you owe IRS back tax – do something!

You do have options if you owe the IRS back tax. The most important thing that you can do is something. Doing nothing is never a viable solution if you owe IRS back tax. With all of the enforcement options available at the IRS disposal, you cannot afford to keep your head in the sand.

If you would like to talk with an experienced Ohio tax attorney about your IRS back tax, call 330-331-7611 or request a free case analysis online today.

- CP 504 Notice IRS Balance Due Notice of Intent to Levy[/caption]

What can the IRS do to me if I owe IRS back taxes?

With a 2019 budget of $11.8 billion and 73,554 full-time employees, the IRS has plenty of resources to collect back tax. Specifically, the IRS may choose to do any of the following to collect tax debt owed to it.- File a notice of federal tax lien against in the public record to notify your creditors of your tax debt - this is a legal claim to your property and it may affect your ability to obtain credit.

- Seize and sell your property such as cars, boats, guns, jewelry, artwork, or real estate.

- Garnish your wages, social security benefits, retirement income, or 1099 income.

- Levy and take your bank accounts - they will literally wipe your balances out and there is little you can do to stop them.

- File civil cases in Federal District Court through the Department of Justice.

- Make criminal referrals to the Department of Justice in certain situations.

What can I do if I owe the IRS back taxes?

Offer in Compromise IRS Back Tax Settlement

An IRS offer in compromise allows you to settle your back tax debt for less than the full amount you owe. The IRS will consider an offer amount based on your income, expenses, and asset equity. Before you submit an offer in compromise, you must ensure that you have filed all required tax returns. If you are self-employed, you must also be current with any required estimated tax payments. If you are in active bankruptcy, you are ineligible to file an offer in compromise until the bankruptcy proceeding are closed. The IRS has a useful tool to see if you are eligible for an offer in compromise based on your income, expenses, and asset equity. It is important to understand that the offer in compromise process is strictly a 'mathematical process' that is based on your ability to pay (i.e. your income and expenses) and your available asset equity. It is not a 'negotiation over the phone' and it is not a quick process. The typical offer in compromise will take 9-14 months from start to finish, assuming the IRS accepts your offer and you do not need to appeal a rejection. If you are going to submit an offer in compromise in an attempt to settle your back tax, you will need two forms: IRS 433-A (OIC) and IRS 656. The IRS 433-A is the Collection Information Statement for Wage Earners and Self-Employed Individuals. This is the form that provides your full financial disclosure to the IRS, including your income, expenses, and assets. It is important that you understand a concept known as 'Collection Financial Standards' before completing this form. For many household expenses (such as food, clothing, housing, utilities, out-of-pocket health care costs), the IRS will allow pre-determined monthly amounts (even if you don't actually pay these amounts). You can increase the likelihood of an acceptance by understanding how to legally maximize your available household expenses. The IRS 656 is the actual Offer in Compromise form that you will use to make your offer to the IRS. On this form, you have to identify the tax (and periods) that you want to include in your offer. Additionally, you will specify your offer amount and how you propose to pay the offer amount. An offer can either be paid as a lump sum (paid in 5 or fewer payments within 5 or fewer months of acceptance) or by period payment (paid in full between 6 to 24 months). Generally, you will be able to pay less by doing a lump sum offer.Temporarily Delay IRS Back Tax Collection - Currently Not Collectible

If you are under a financial hardship (generally, this means that you have just enough income to handle your allowed household expenses), the IRS can 'close' your collection account temporarily. The tax debt doesn't go away - but the IRS will stop all collection activities against you while in this status (including garnishments). Generally, if the back tax is old, you may be able to stay in this 'temporary' status all the way to the statute of limitations and the tax debt will be permanently written off by the IRS. The statute of limitations is typically ten years from the date of assessment (this is also the date that your tax return is processed by the IRS). It is important to understand that the IRS can 'check in' on you every couple of years to see if your financial situation has improved. The IRS will also take any tax refunds you are entitled to. To avoid this, make sure that you update your paycheck federal income tax withholdings to have less taken out each paycheck so that you have a minimal refund for the IRS to take. With a 'currently not collectible' status, the IRS will almost always file a tax lien against you. Unfortunately, there is not much you can do to avoid this if you are asking the IRS to temporarily delay collection efforts against you.Long Term IRS Streamlined Installment Agreement

The IRS has payment plan arrangements that can be made to pay your back tax within an extended timeframe. The most popular payment plan with the IRS is the streamlined installment agreement. The payment plan is for 72 months and the payment amount is based on the assessed and accrued balance of your tax liability divided by 72. Generally, to get this amount, look at the last notice that you received (such as the CP504 notice). Take this amount (for each tax year that you have received a notice for) and divide by 72. That amount represents your monthly payment amount. You can even setup your installment agreement online through your IRS account. The streamlined installment agreement is generally available for balances of $50,000 or less. If your balance is more than $50,000, but less than $250,000, you may still be able to setup an installment agreement without providing financial disclosures under the IRS COVID People First Initiative. Your proposed monthly payment amount, however, must full-pay the entire balance (including interest and penalties) before the statute of limitations date. Once your installment agreement is established, consider requesting a first-time penalty abatement. You can save thousands of dollars this way. If you did not owe back tax for three years prior to the year that penalties were assessed for, you likely qualify for a first-time penalty abatement. You can ask for this over the phone with the IRS at 1-800-829-7650 - call early, though, as wait times generally exceed 1-2 hours.Partial Payment Installment Agreement

If you do not qualify for a temporary delay in collection as 'currently not collectible' and you cannot afford the streamlined installment agreement (i.e. the tax liability divided by 72), an alternative may be the partial payment installment agreement. Under this arrangement, the IRS will review your financial information (provided to the IRS generally through a 433-A or a 433-F) and determine what you are able to pay (including through any asset equity). Likely, under this arrangement, your monthly payment amount will never full pay the tax liability before the statute of limitations. At that point of time, the remaining tax balance will be written off by the IRS. It is possible to have a partial payment installment agreement for a large tax liability with a minimal monthly payment (we have seen them as low as $10.00 per month). Under this arrangement, however, you have to ensure that you do not add additional back tax as it will cause your agreement to default. Similarly to the 'currently not collectible' status, if you are due a tax refund, the IRS will take the tax refund, so you will want to adjust your withholdings so as to not have a tax refund.Full Pay with Penalty Abatement

If you have the ability to full pay your back tax balance, then you likely to not qualify for any form of settlement, such as the offer in compromise. However, all is not lost. You can likely still save significant money in the form of tax penalties. As discussed above, if you had a clean compliance history for the preceding three years (from the year with the tax balance), you can simply call the IRS and ask them for a first-time abatement of your tax penalties for the year with the balance that you are full-paying. Technically, they will want you to full-pay the balance first and then request a refund through Form 843, but many of the agents will grant the first-time abate if they know you plan on full-paying your balance. Even if you do not qualify for first-time abatement, you may want to consider a 'reasonable cause' abatement if there were good reasons why the tax was not paid on time. Generally, tax penalties are well into the $1,000's - sometimes more. It is important to note that interest cannot be abated - only penalties (such as the failure-to-file penalty and the failure-to-pay penalty). However, interest that has accrued on the penalties will be abated if a penalty abatement is granted. If you are going to full-pay your IRS back tax balance, you should definitely send the payment electronically through the IRS Direct Pay website. Do not send a check as it is not reliable. If you must send a check (again - not recommended), make sure that your social security number and the tax year you want to apply the payment to is on the memo line of the check.If you owe IRS back tax - do something!

You do have options if you owe the IRS back tax. The most important thing that you can do is something. Doing nothing is never a viable solution if you owe IRS back tax. With all of the enforcement options available at the IRS disposal, you cannot afford to keep your head in the sand. If you would like to talk with an experienced Ohio tax attorney about your IRS back tax, call 330-331-7611 or request a free case analysis online today." target="_blank">

0 Comments